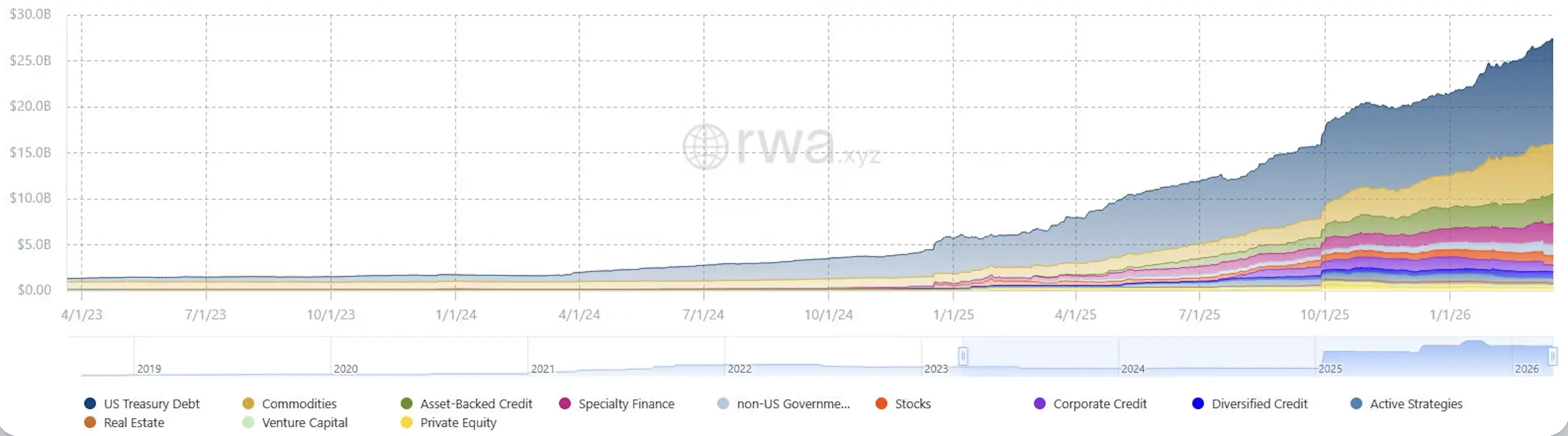

While prices continue to stumble and metrics across the broader crypto market remain largely stagnant, the uptrend in tokenized assets shows no signs of slowing. From around $5 billion in 2022 to more than $26 billion in March 2026, the market for tokenized real-world assets outside of stablecoins has nearly doubled since the end of 2024 alone. The picture becomes even more striking when stablecoins are included. They now bring the total on-chain RWA market to roughly $300 billion and reached $33 trillion in transaction volume in 2025. While the rest of the crypto market remains sluggish, tokenization of real-world assets is emerging as one of the few segments showing genuine adoption.

“Distributed Value” vs. “Represented Value”

Anyone looking into real-world assets quickly runs into very different market size estimates. That is mainly because many dashboards mix together two distinct categories: Distributed Value and Represented Value.

Distributed Value refers to assets that have actually been issued on a public blockchain, are held in wallets, and can be transferred according to the rules of that network. This category is especially relevant for the crypto market because it reflects real on-chain usage, potential secondary liquidity, and DeFi compatibility.

Represented Value is much larger, but it works differently. In this case, assets are mapped or registered on-chain, often through institutional or permissioned networks. That does not automatically create freely tradable tokens.

The Distributed Value of the RWA market excluding stablecoins currently stands at around $27 billion. Represented Value is above $342 billion.

Stablecoins dominate the market

As strong as growth in the non-stablecoin RWA market appears, stablecoins still remain the dominant force. At around $300 billion, they account for roughly 92% of all tokenized real-world assets. The usage numbers are even more impressive. In 2025, stablecoin transaction volume reached about $33 trillion, up 72% from the previous year. In the fourth quarter of 2025 alone, stablecoin transactions totaled $11 trillion.

USDT and USDC are moving apart

One of the most interesting developments is happening at the top of the stablecoin market. For the first time, the two largest stablecoin issuers, Tether and Circle, are structurally moving in opposite directions.

Tether’s USDT remains number one with a market capitalization of around $174 billion, but it is coming under increasing pressure. Circle’s USDC has now reached $76.24 billion and continues to grow. On a yearly basis, that represents an increase of 72%. Circle is benefiting from stronger regulatory alignment, broad institutional distribution, and growing multi-chain adoption.

The core driver of this divergence is regulation. In Europe, MiCA is now fully in force. Based on currently available information, among the ten largest stablecoins, only USDC fully complies with MiCA requirements. That is reshaping the market. USDT continues to dominate in unregulated markets, while USDC is establishing itself as the preferred stablecoin in regulated environments.

RWA market outside stablecoins

The largest segment of the non-stablecoin RWA market is now tokenized US Treasuries and money market funds. This category has grown to roughly $10 billion, making it one of the most successful areas in the sector.

The logic is simple. Institutional investors are looking for liquid, low-risk, yield-bearing instruments that can be settled digitally and almost in real time. Among the leading products is BlackRock’s BUIDL, with $2.53 billion in assets under management. It is considered the largest tokenized fund in the market and has already distributed more than $100 million in actual Treasury yield to on-chain investors. USYC from Circle and Hashnote stands at around $1.90 billion and briefly overtook BUIDL in early 2026.

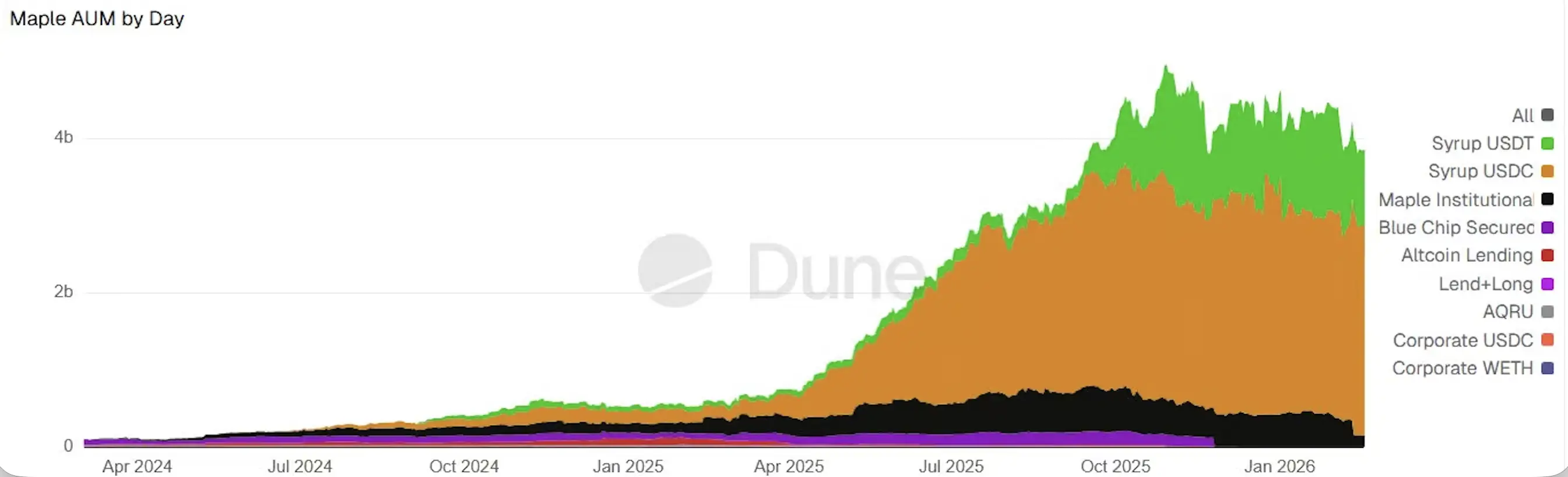

Maple drives private credit growth

Growth is also visible in other areas, especially private credit. This segment now accounts for more than $5 billion, representing a substantial share of the non-stablecoin RWA market. Platforms such as Centrifuge and Goldfinch remain important players, but the space is clearly dominated by Maple Finance, which recorded massive growth over the past year.

At the same time, this category also concentrates risk. Wherever credit is created, defaults, restructurings, and operational counterparty risks remain. Tokenization does not change the fact that poor credit quality is still a problem on-chain. So far, however, the sector has remained remarkably stable.

Commodities and equities as growth areas

Given the powerful rally in precious metals, it is hardly surprising that tokenized commodities are also growing. Tether Gold and Paxos Gold dominate this segment. The total tokenized commodities category now stands at around $7.6 billion.

Still small but strategically very interesting are tokenized equities. This market currently stands at around $1 billion. Relative to the global stock market, that is tiny, but momentum is clearly building. The US Securities and Exchange Commission has now approved a rule change allowing Nasdaq to support trading in tokenized equities. Participants in a pilot program by the Depository Trust Company will be able to settle stock trades in tokenized form, while using the same order books, execution priority, and shareholder rights as traditional securities. That is an important step, because tokenized equities have so far mostly been accessible only through specialized platforms and often outside the US market. If major exchanges and core market infrastructure begin integrating these products into regulated workflows, the RWA sector will move even more strongly into institutional focus.

Ethereum and Canton dominate

There is also a clear split when looking at which networks host RWAs. For Represented Value, Canton dominates by a wide margin. The network is designed for institutional use cases and is most relevant where regulated market participants want to bring existing financial processes onto blockchain rails without fully entering open crypto markets.

That large Canton figure therefore says more about traditional finance’s growing interest in tokenized infrastructure than about how much of that value is actually circulating in public on-chain markets. For Distributed Value, Ethereum is the clear leader with around $15.5 billion. It is followed by BNB Chain, Liquid Network, and Solana. Ethereum benefits from its position as the standard network for tokenized funds, Treasuries, private credit, and commodities. It is also supported by the fact that many institutional issuers and infrastructure providers already rely on Ethereum-compatible standards, established custody solutions, and existing DeFi integrations.

That combination of market acceptance, technical maturity, and compatibility with existing capital markets makes Ethereum by far the most important blockchain for tokenized assets today.

Regulation and liquidity remain unfinished business

As strong as product and infrastructure progress has been, the open challenges are just as clear. The biggest remains liquidity. Many issuers are not tokenizing assets to build actively traded markets, but mainly for capital raising or operational efficiency. Secondary markets in many segments remain thin. In other words, tokens exist, but there are often still too few buyers and sellers to create truly deep markets.

Regulatory uncertainty also remains unresolved. In the US, the GENIUS Act in 2025 was a milestone for stablecoins, creating the first comprehensive framework for payment stablecoins. But the CLARITY Act is still pending. In Europe, MiCA provides structure, but it also raises barriers to entry and increases global fragmentation.

Overall, the market has reached a point where the broad direction is no longer really in doubt. The open question now is how quickly the next stage of development will materialize and which players will benefit the most. Given the success of perpetual futures for equities and commodities so far, the perps DEX Hyperliquid could ultimately emerge as one of the biggest winners from the convergence of TradFi and crypto.